Évaluation environnementale du budget : Revue des expériences internationales

I4CE a analysé 10 « budgets verts » à travers le monde afin d’identifier les conditions méthodologiques et procédurales pour que cet exercice soit vraiment utile, et la France en remplit beaucoup. Mais même bien utilisé, cette évaluation ne permet pas de savoir si le budget d’un pays ou d’une collectivité est cohérent avec son ambition climatique.

De nombreux pays ont fait des évaluations environnementales de leurs budget, et cette étude d’I4CE fait le point sur les bénéfices attendus et les critères à respecter pour les réaliser : recenser les mesures défavorables à l’environnement, ne pas s’intéresser uniquement aux mesures qui ont pour objectif premier l’environnement, inscrire ces exercices dans le temps long et dans les processus administratifs existants…

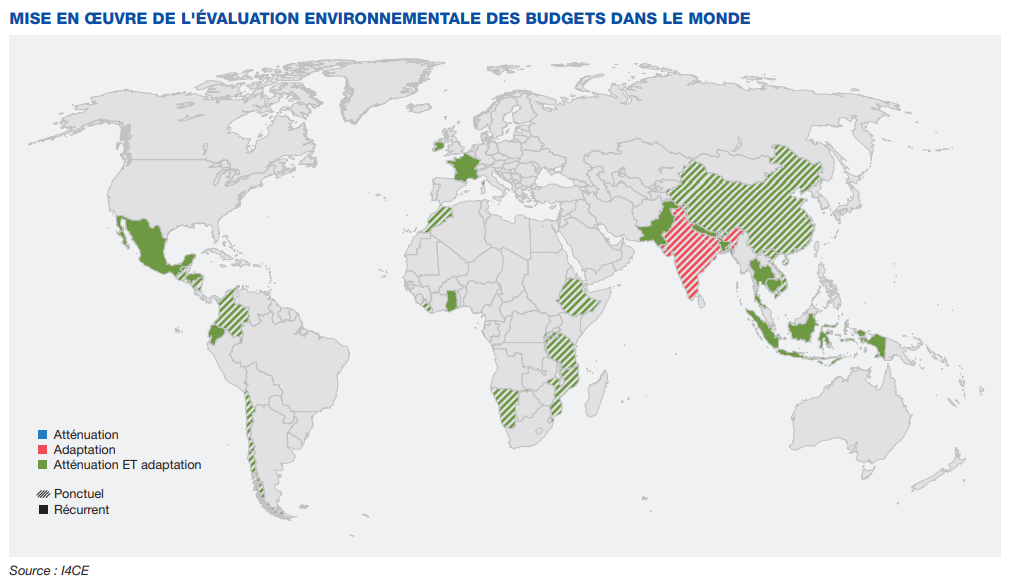

Les questions climatiques et environnementales touchent tous les aspects de la vie économique d’une nation. Prenant acte de cette réalité, les ministères des Finances sont de plus en plus nombreux à mettre en place des outils pour faciliter et optimiser la prise en compte de l’environnement dans les décisions budgétaires, outils dits «de budgétisation verte ». L’Évaluation Environnementale des Budgets (EEB) est l’un d’eux, qui vise à mettre en évidence toutes les mesures budgétaires liées à une ou plusieurs dimensions de l’action environnementale, telles que le changement climatique, la biodiversité ou la dégradation des sols.

Cette revue fait le point sur l’expérience existante pour répondre à deux questions : quels sont les bénéfices attendus de ces outils ? A quelles conditions sont-ils réalisés ? Elle s’appuie sur l’expérience d’une grosse vingtaine de pays, et de plusieurs institutions internationales du développement (PNUD, BID, Banque Mondiale, OCDE), au moyen de revues bibliographiques et d’une série importante d’entretiens au sein des ministères et parmi les chercheurs, consultants etc. qui les ont accompagnés dans ces évaluations. 10 études de cas (8 d’Amérique latine + Indonésie et France) ont été examinées en profondeur, leurs conclusions et comparaisons étant rassemblées dans une annexe méthodologique à ce rapport. L’étude se concentre notamment sur les différences entre les évaluations « minimales » et les évaluations exhaustives, constatant que les importants bénéfices supplémentaires associés à une évaluation exhaustive justifient amplement l’effort additionnel associé.

Dans tous les cas, de tels choix doivent être faits très en amont, car ils structurent fortement tout l’exercice d’évaluation. Les éléments différenciants entre évaluations simples et complètes se divisent en deux catégories :

- les critères méthodologiques : pour être efficace, une EEB doit travailler sur un périmètre élargi, évaluer les dépenses mais aussi les taxes, prendre en compte les impacts des mesures et non seulement l’intention, recenser les mesures défavorables à l’environnement… Viser à évaluer la cohérence du budget avec les objectifs nationaux, et pas seulement l’effort environnemental.

- les critères de processus : les effets d’une EEB se font pleinement sentir à deux conditions :

– une excellente appropriation nationale : l’EEB doit avant tout répondre à un besoin spécifique au contexte, clairement identifié en amont, au moyen de ressources internes. Elle doit aussi s’inscrire dans la culture et les processus administratifs existants, en cohérence avec les autres outils nationaux de budgétisation verte.

Cliquez sur ce bouton pour voir l’image

– une inscription dans le temps long : il ne s’agit pas d’un exercice à réaliser une fois, mais d’un effort à maintenir dans la durée. C’est bien sûr nécessaire pour mesurer l’amélioration ou la dégradation des indicateurs, et corriger la trajectoire nationale « en temps réel » ; mais c’est aussi important pour donner le temps à certains processus de se mettre en place. En particulier, c’est en maintenant l’exercice dans le temps qu’on pourra dépasser les considérations sur les seuls volumes monétaires et ouvrir le débat sur l’efficacité environnementale des mesures ; c’est aussi dans le temps que peut s’installer une vraie dynamique d’échange, d’acculturation et de montée en capacité des différents acteurs – or c’est à travers ces changements de fond qu’une EEB a le plus d’impact.

Aux conditions énumérées ci-dessus, une EEB est utile à la fois pour les résultats d’analyse qu’elle produit, et par le processus même qui conduit à ces résultats. En premier lieu, en améliorant la transparence sur l’action publique, sur des thématiques où les attentes du public sont élevées. Ensuite, en instaurant un dialogue interministériel qui permet aux ministères des finances et ministères techniques de s’approprier, dans leur périmètre, un sujet complexe vu sa nature très transversale. Enfin, en informant les arbitrages budgétaires avec des outils simples sur des sujets qui ne le sont pas, agrégeant des informations potentiellement éparses et faisant ressortir les co-bénéfices ou effets indésirables de mesures ou paquets de mesures n’ayant pas tous un objectif climat affiché. Enfin, elles fournissent des instruments de reporting appréciés des financeurs internationaux privés (Obligations vertes) ou publics (banques de développement), même s’il faut alors être vigilant car l’incitation financière peut biaiser l’évaluation. Pour autant, il ne faut pas trop attendre de cette évaluation : c’est un outil important et pertinent pour la politique budgétaire d’un gouvernement affichant des objectifs environnementaux, mais ce n’est qu’un outil, assez technique par ailleurs. Il n’est utile qu’au service d’une volonté politique forte, et au sein d’un écosystème d’outils d’aide à la décision et la planification.

{kind=link}