The Bankability Test: Unlocking Bank Credit for European Cleantech

On the cusp of the Age of Electricity, Europe is on a mission to both strengthen industrial competitiveness and accelerate decarbonisation. The European Commission’s Clean Industrial Deal serves as the blueprint to deliver this ambition. Yet, its implementation necessitates unprecedented levels of private investment. I4CE estimates Europe’s annual clean energy investment needs at €878 bn to meet the bloc’s 2030 targets (I4CE, 2026a). Europe’s banks are central to footing that bill – bank loans are the driving force of the economy, accounting for over 90% of GDP (ECB, 2026a). Despite sufficient bank lending capacity, many European cleantech scale-ups struggle to secure long-term bank loans. The barrier is not simply a shortage of capital, but a shortage of bankable projects.

The financing gap is most acute during the growth stage.

The so-called ‘valley of death’, where firms typically seek between €30 mn and €100 mn to fund development costs. Part of the problem is well-documented: only 20% of European climate tech funds focus on growth financing, leaving a real equity gap (World Fund, 2026). But limited bank lending reflects weak project bankability. Banks are unwilling to lend before stable revenues are secured, as higher project risks also increase banks’ regulatory capital costs. The result is that commercially promising technologies stall before they can scale.

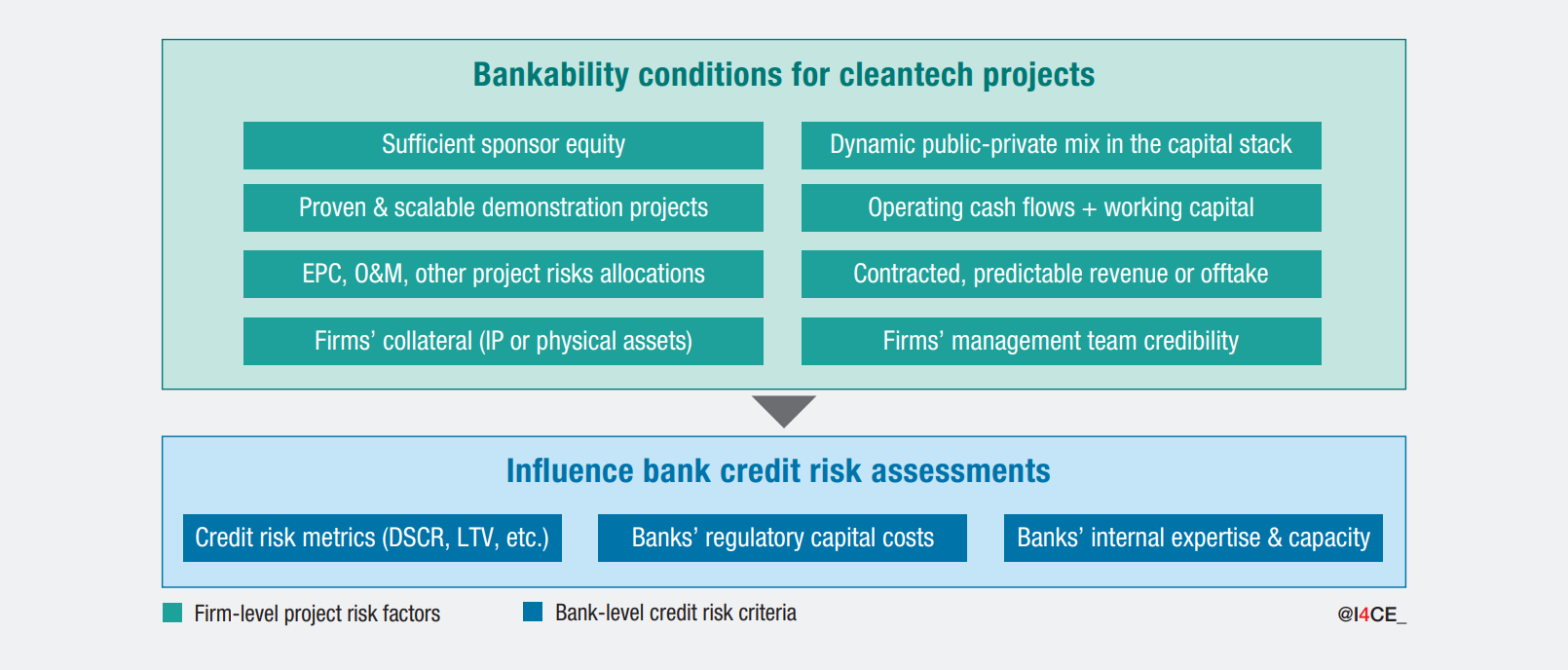

Figure 1 – Cleantech bankability is based on several underlying conditions that determine creditworthiness

Solving for bankability requires solving for project credit risk.

Equity investors assess investability to finance growth based on expected returns over relatively short investment horizons. Banks, however, assess project bankability against a robust risk framework, including the offtake credibility, the equity capital stack, the collateral (if any), and the management team, among others (Figure 1). Successful cleantech firms that mitigate these risks before Final Investment Decision (FID) can better access bank project finance loans, which financed only 11% of European cleantech investments in 2024 (World Fund, 2026). Treating cleantech scale-up financing as primarily a capital shortage problem masks the more fundamental challenge of unbankable project credit risks.

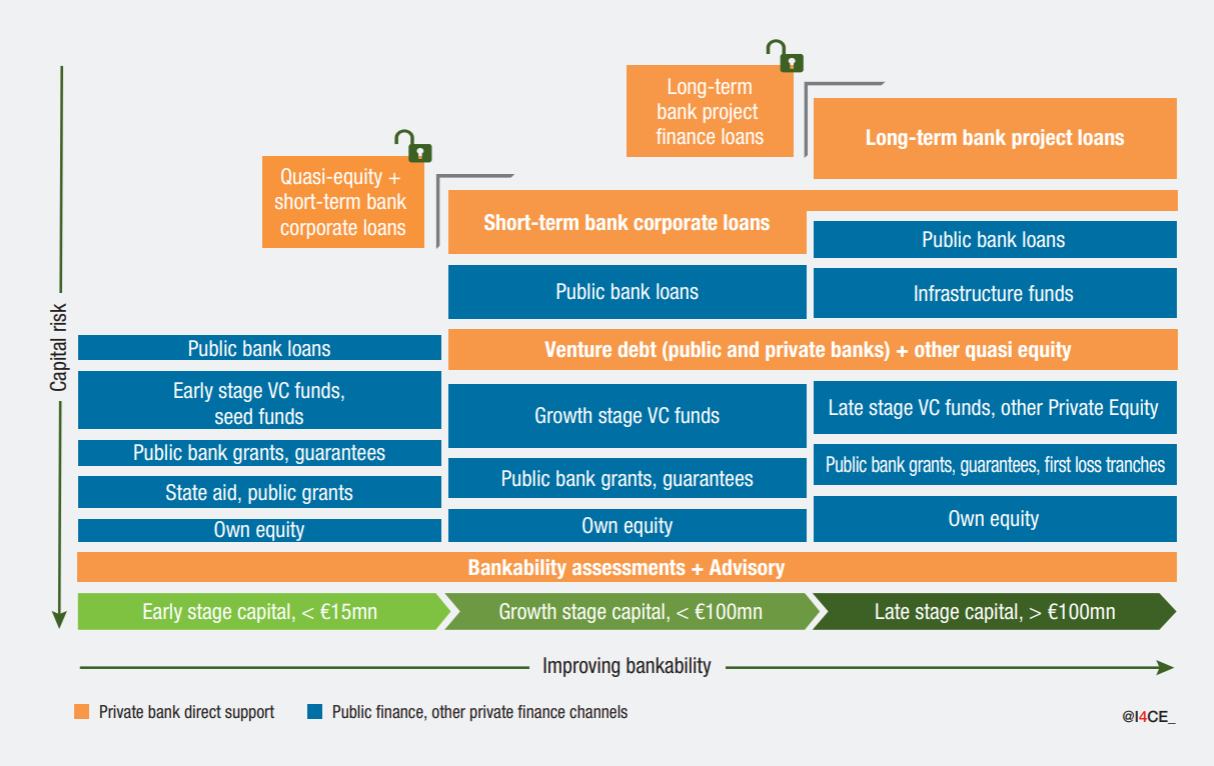

Figure 2 – Private bank’s direct leading role unloacked at each stage of the cleantech fundraising cycle

Prudential capital requirements are a real but secondary constraint.

Capital relief for cleantech lending already exists under the Infrastructure Supporting Factor (IFS), which is used extensively by large banks. However, lending decisions are driven more by underlying project creditworthiness, which exceeds the benefit of capital incentives on banks’ profitability. European banks’ capital positions are already strong, with dividend payouts back to pre-pandemic levels. Policymakers should be cautious when treating renewed calls to reduce capital requirements on competitiveness grounds – it is likely to have little impact on boosting cleantech lending. Bank-level supervisory tools such as prudential transition plans and supervisory dialogues, if used proactively, could prove more useful in supporting bank practices towards European decarbonisation priorities.

The bank credit pipeline is flowing to the few bankable cleantech projects that overcome key risk hurdles.

The policy task is to expand that pipeline. Drawing on the example of floating offshore wind, this research paper identifies the key conditions that improve cleantech bankability to access both short and long-term bank loans. Policymakers should respond with targeted early-stage public derisking tools, stronger equity support and local ecosystem clusters to help more projects reach bankability faster for the European clean industrial transition.