Green reindustrialisation in France: reality, reasonable ambition or pipe dream?

The global race for clean technology is on. China is consolidating its industrial lead, the United States is playing an unpredictable game with subsidies and tariffs, and mounting geopolitical tensions are redrawing global supply chains, laying bare Europe’s strategic dependencies in energy and industry.

Faced with this reality, France and the European Union face a fundamental choice: adapt or fall behind. Building a decarbonised, “Made in Europe” industrial base is not one policy option among many – it is a prerequisite for economic and energy sovereignty in the decades ahead.

But translating this ambition into practice is harder than passing legislation or setting targets. Building competitive domestic value chains for clean technologies means simultaneously transforming deeply entrenched industrial structures, and developing entirely new ones around breakthrough technologies. This I4CE report takes stock of where France actually stands on that journey, through the lens of three flagship cleantech industries: electric vehicles and batteries, green steel, and electro-synthetic aviation fuels (eSAF).

So what is the real picture? Gigafactories have been inaugurated, decarbonisation roadmaps announced, and synthetic fuel projects are multiplying. France’s green industrial policy has delivered real momentum. But how effectively is it actually building the integrated, competitive value chains that would make this transformation durable?

That is the central question this report sets out to answer. The three sectors were chosen precisely because they represent very different stages of industrial maturity: from operational gigafactories to green steel and eSAF projects still awaiting final investment decisions. Critically, for each sector the analysis looks at both supply-side development and demand dynamics.

What emerges is a finding that cuts across all three cases: a widening gap between project announcements and the actual construction of value chains. The first gigafactories have been built, but upstream supply (critical raw materials, precursors, recycling) remains heavily exposed to Chinese dominance; green steel is moving thanks to first secure investment decisions but still lacks a sufficiently clear and structured demand; and eSAF projects are advancing through engineering studies, but cannot clear the financing hurdle without long-term offtake commitments. In each case, it is the neglected steps of the value chain that leave the door open to outside competitors.

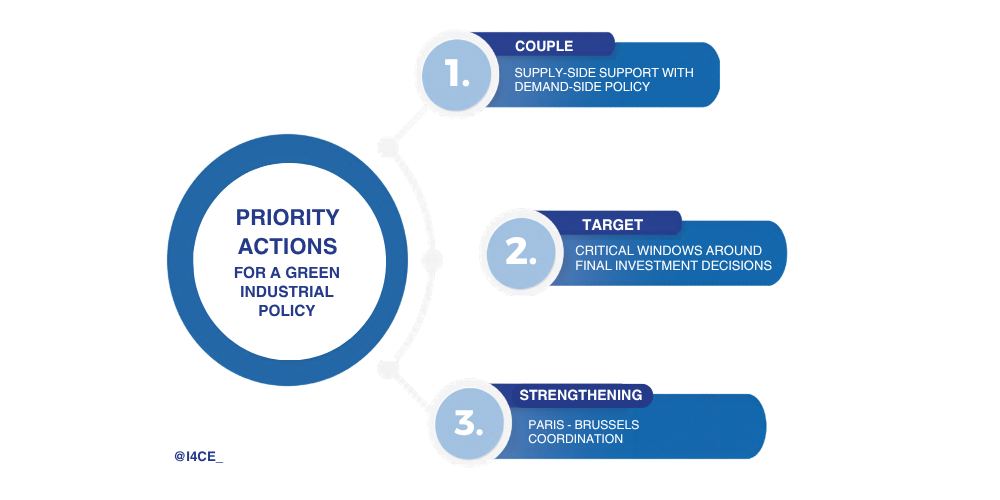

The report identifies three priority levers to address these bottlenecks. First, supply-side support must be coupled with active demand-side policy through binding low-carbon procurement standards in public infrastructure and mandatory sectoral requirements for private buyers. Second, public policies must tackle the critical window around final investment decisions, combining stable sectoral targets with revenue certainty mechanisms, like contracts for difference, to underwrite the ramp-up of first-of-a-kind facilities. Third, France needs tighter coordination between Paris and Brussels, through dedicated taskforces for strategically critical projects and a more assertive French role in shaping European financing instruments and trade defence measures.

Green reindustrialisation in France is underway. But the line between industrial success story and missed opportunity remains, for now, uncomfortably thin.

This I4CE report is available in French. The case study on the French eSAF sector has been translated and adapted to inform the ongoing European debate on ReFuelEU aviation.

With France as Europe’s single largest eSAF project hub, with roughly 30% of the continent’s planned capacity and some of its most advanced projects, what happens in France over the next 18 months will largely determine whether Europe will be able to meet build out the value chain for an emerging cleantech and meet its first blend-in mandates.

The barriers France faces are structural and shared, with no European large-scale project having yet reached a final investment decision. Understanding why France, despite benefiting from structural advantages, has not yet broken that deadlock is therefore essential reading for anyone working on eSAF at European level.

This case study examines France’s emerging eSAF sector, the announced projects, market dynamics and public support schemes, and puts forward concrete recommendations to help the market take off before the window of Opportunity closes.