What role for financial regulation to help the low-carbon transition?

States and more generally public authorities will not finance the transition to a low-carbon and climate-resilient economy on their own. Private financial actors have a key role to play and, over the past decades, they have taken numerous initiatives to promote “responsible investment” and “sustainable finance”. However, the impact of these initiatives is far from commensurate with the climate challenge, , and financial regulation must play a role. This I4CE study analyses the different objectives that regulators can pursue to help the financial sector respond to the climate urgency, and provides an overview of the instruments at their disposal. It also highlights the challenges of implementing these instruments and identifies those that need to be used in the short term and those that need more time to be implemented.

Different and more or less controversial objectives

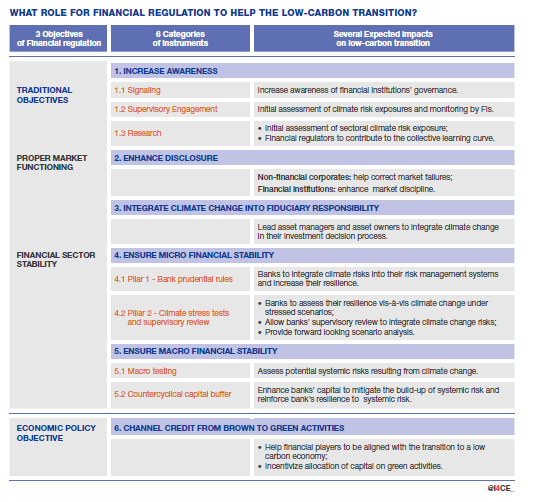

Ensuring a proper market functioning and financial stability are the traditional objectives of financial regulation, and there is now broad agreement among regulators that regulation needs to evolve to better address climate issues, through the integration of climate risks for instance. However, these developments can be seen as insufficient in view of the climate urgency and the question is whether financial regulation could and should also pursue macro-policy objectives such as redirecting financial flows towards “green” activities at the expense of “brown” activities. This is a highly controversial debate, and one that should not be considered as closed: financial regulation has already been extended in many countries to economic policy areas such as consumer protection and financial inclusion.

A variety of regulatory instruments are available

These instruments can be grouped into 6 main families:

– Tools that increase financial actors’ awareness of climate risks and help understand the implications of climate change ();

– The ones ensuring the disclosure of environmental and climate-related information;

– Tools that integrate climate criteria into the fiduciary responsibility, to go beyond the short-term maximisation of financial returns ;

– The one strengthening the microprudential stability, by reinforcing climate risks management and individual actor’s resilience, as for instance, for banks, this could mean integrating climate-related risks into prudential regulation;

– Tools safeguarding macro-prudential stability, as climate macro stress-tests

– Tools that Promote investment allocation according to economic policy objectives, as : State- directed Priority Sector Lending program (e.g. India), or Green Finance Guidelines (China).

Click on this button to see the image

Implementation challenges and priorities

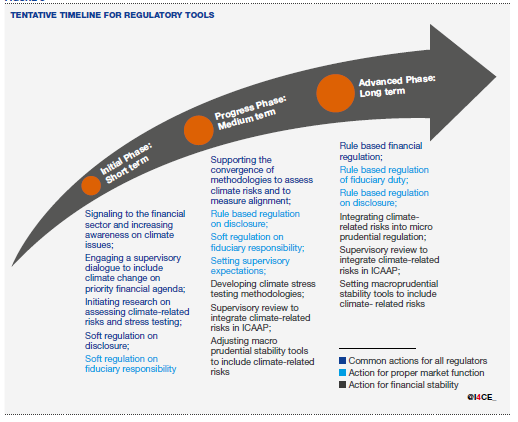

The instruments to be used by regulators obviously depend on the objective pursued. If we stick to the traditional objectives of financial regulation, it is therefore necessary to use both the tools that strengthen financial stability and those that serve to improve transparency and disclosure. But it will take time to fully integrate climate-related risks into financial regulation. Measures that can be taken in the short term and launched without further delay include, for example, raising awareness, set supervisory expectations, enhance disclosure and strengthen the supervisory processes. Some regulatory measures should be among the priorities of supervisors but are not ready yet to be implemented: climate stress tests, for example, are only developed by a few leading supervisors who are still in the initial stages of development. Other measures, finally, will require more time. More challenging is integrating climate-related risks into rules-based prudential regulations , such as banks’ capital requirements., This will require widely accepted risk metrics and robust risk assessment methodologies to adress the “radical uncertainty” of climate change, as well as a certain level of international cooperation to implement them.

The controversial use of financial regulation to influence the allocation of investment also raises issues that are as much “political” as they are “technical”. Could financial regulation usefully complement economic policy measures to address certain market failures? How can possible conflicts of interest between traditional and economic policy objectives be tackled? Should the mandate of financial regulators be modified to allow them to pursue economic policy objectives in addition to their traditional objectives? This is clearly an area that deserves further research to better inform this debate.

Click on this button to see the image

Julie Evain explains, in this two minutes video, the main lessons of this study.

A video to watch for a first discovery of the issues at the crossroads of financial regulation and the fight against climate change:

Disclaimer

This study has been elaborated with the financial support of Climate KIC.

However, the views expressed in this report are those of the authors and do not reflect the official opinion of Climate-KIC.

![]()

A first version of the report was drafted as a contribution to a European project funded by Climate KIC to help develop the network of Financial Centres For Sustainability (FC4S) in Europe. The report aimed to support these centres in assessing their situation and developing their strategy

{kind=link}

{kind=link}