Les comptes mondiaux du carbone en 2019

Les comptes mondiaux du carbone en 2019 d’I4CE présentent les principales tendances concernant la mise en oeuvre des politiques de tarification explicites du carbone dans le monde en 2019.

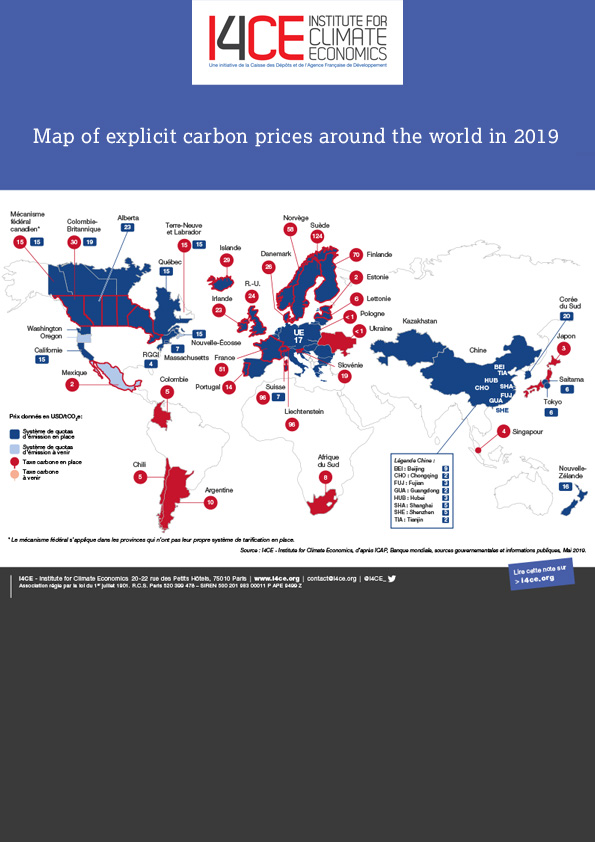

Les 5 tendances de 2019

- Au premier mai 2019, 25 taxes carbone et 26 marchés de quotas échangeable étaient en fonctionnement à travers le monde. Les juridictions couvertes par un ou plusieurs prix explicites du carbone représentent environ 60 % du PIB mondial.

- La tarification du carbone progresse à l’échelle mondiale, malgré des revers locaux. Au Canada, les élections provinciales en Ontario et Alberta ont entraîné l’annulation des systèmes de tarification locaux ; en parallèle, la tarification fédérale est entrée en vigueur pour toutes les provinces n’ayant pas leur propre prix du carbone. En France, le mouvement des gilets jaunes a poussé le gouvernement à geler sa taxe carbone au niveau actuel de 51 USD par tonne, sans toutefois la révoquer. Les marchés de quotas chinois et mexicain devraient démarrer en 2020 leur opération effective.

- Les instruments de tarification du carbone ont généré 45 milliards de dollars US (40 milliards d’euros) en 2018, contre 32 milliards en 2017 et 22 milliards en 2016. Cette hausse est principalement due à l’augmentation des prix du marché européen, passés de moins de 10 dollars avant 2018, à plus de 25 dernièrement.

- En 2018, 52 % des revenus du carbone provenaient des taxes, contre 48 % des marchés de quotas. Les revenus sont majoritairement intégrés au budget général, ou fléchés vers des projets environnementaux.

- Plus de 75 % des émissions régulées par une tarification du carbone sont couvertes par un prix inférieur à 10 dollars US (8 euros). Pour s’aligner sur une trajectoire 2°C compatible avec l’Accord de Paris tout en encourageant la croissance économique, la Commission de haut niveau sur les prix du carbone présidée par les économistes Stern et Stiglitz recommande des prix du carbone compris entre 40 et 80 dollars US par tonne de CO2 en 2020, puis entre 50 et 100 dollars US par tonne de CO2 en 2030, partout dans le monde.

Principales sources du rapport et liens pertinents :

- “State and Trends of Carbon Pricing 2019”, World Bank, https://openknowledge.worldbank.org/handle/10986/13334

- ICAP Status report 2019: https://icapcarbonaction.com/en/icap-status-report-2019

- Working paper OCDE https://www.oecd-ilibrary.org/taxation/the-use-of-revenues-from-carbon-pricing_3cb265e4-en

- Base de données PINE de l’OCDE https://pinedatabase.oecd.org/

- Carbon pricing dashboard de la Banque Mondiale https://carbonpricingdashboard.worldbank.org/

- ETS Map de ICAP : https://icapcarbonaction.com/en/ets-map