Non-Financial Reporting by companies and Scenario Analysis: be cautions with Standardization

A few months ago, the European Commission launched a consultation on the revision of the Non-Financial Reporting Directive. The issue at stake is to strengthen the obligation for 6,000 large companies to communicate publicly on how they deal with major societal issues, such as climate change and low-carbon transition. For Romain Hubert of I4CE, reporting must be strengthened in particular on the scenario analyses that companies conduct to identify the risks and opportunities of the transition. But what exactly should they communicate?

Here are our recommendations, based on our latest research report, for mandatory reporting on scenario analysis of transition risks and opportunities.

Scenario analysis, an essential exercise

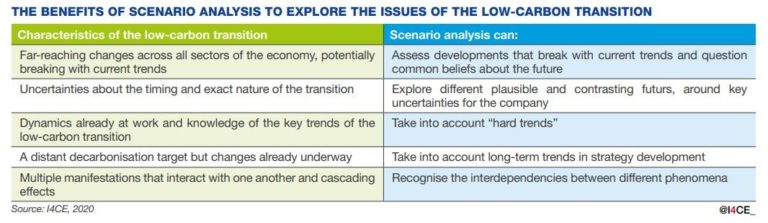

In order to drastically reduce their greenhouse gas emissions and achieve carbon neutrality, all sectors of the economy will have to undergo a profound transformation. This transition to a low-carbon world exposes companies to strategic risks and opportunities in their business environment, which are all the more difficult to apprehend because there are many uncertainties about the extent of the efforts that will be implemented for the transition, their timing and their modalities.

In this context, “scenario analysis” is proving to be a very useful tool for companies to explore the concrete challenges of the low-carbon transition and build a strategy that is resilient to possible futures. This exercise is moreover recommended by the TCFD expert group, and some companies – too few – are already conducting this type of analysis. Scenario analysis is useful to the companies themselves, and it is also useful to their financial stakeholders: bankers, investors and others. Financial actors need to know more about these business-driven analyses, to measure how the companies they finance also expose them to transition-related risks and opportunities.

Click on this button to see the image

Reporting requirements must be strengthened

Corporate non-financial reporting is a possible channel of communication between companies and financial players on scenario analysis, as TCFD points out. However, the directive that frames this reporting at the European level, the NFRD for Non-financial reporting directive, only mentions this type of analysis in its non-binding guidelines. Companies are therefore simply invited to address the subject of scenario analysis in reporting to their financial stakeholders, without being obliged to do so. The revision of the NRFD is an opportunity to change this.

The reporting requirement is relevant first and foremost to stimulate companies to implement scenario analysis and make decisions that improve the resilience of their strategies. Indeed, we see that too few companies are currently implementing scenario analysis. Yet many resources exist to guide companies in this strategic approach, within the means they can devote to it. They can rely, for example, on the report that I4CE has published to help companies familiarise themselves with low-carbon transition scenarios, or on our brand new practical guide on scenario analysis, which presents methodological sheets, online tools, sector-based prospective work, etc.

The reporting obligation is also necessary to help companies take the step of public communication on these analyses. Many of them are struggling with the issue of confidentiality associated with this analysis of strategic interest. However, in writing our practical guide, we have noted that some companies already include elements on this approach in their reporting. It is therefore necessary to play down the issue of confidentiality! Companies need to take things into account. They can take stock of the information they already disclose, and think about the selection of information and presentation formats that will allow them to communicate the important points of the analysis without betraying their confidentiality issues.

Be aware of the standardization of reporting on scenario analysis

The reporting obligation on scenario analysis therefore seems to us to be necessary … In concrete terms, what should companies communicate to their financial stakeholders? Financial stakeholders tend to ask for non-financial information that is comparable between companies, and the Commission suggests a form of standardisation of non-financial reporting. But when it comes to reporting on scenario analysis, we must be wary of standardisation at all costs!

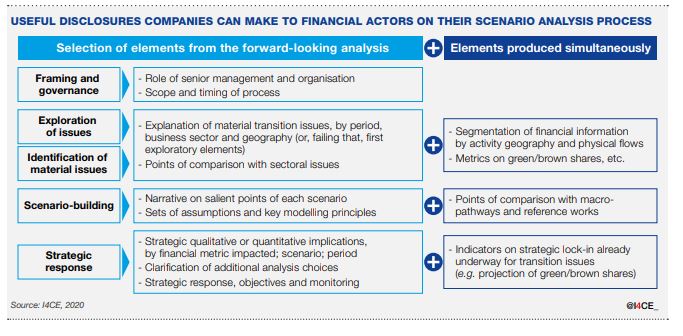

Our report shows that financial players are above all interested in understanding a company’s approach and in assessing the soundness of its approach. How far along are companies in taking into account the challenges of the low-carbon transition? How does it determine its key “material” issues? How does it explore its strategic challenges in the near and distant future? Does it provide an adequate strategic response? In order to do so, the standardisation of reporting should include the obligation to systematically evoke a certain number of aspects of scenario analysis (see table below). They should be communicated in stages according to the company’s rate of progress in its analysis process.

Thus, it is particularly useful for the company to communicate from the outset on the framing phase of its approach, in order to explain how it is building a capacity to integrate prospective analysis into its strategic decision-making. This may be a timetable for implementation, with the different stages, objectives and roles of the people involved – particularly management and the Board of Directors, and the link with the usual processes that feed into strategic thinking.

Note that financial actors will appreciate if the company also provides additional information, such as points of comparison with known work (e.g. how the company’s scenarios relate to known IEA scenarios in finance, or to the four major transition narratives formulated by the NGFS).

Click on this button to see the image

What should not be standardized, however, are the scenarios to be used by companies. It would be counterproductive to impose standardised scenarios on them, on which they should base their strategic decisions. This temptation is great because common scenarios would bring comparability to the analyses of the multiple companies that financial players must examine. But a meaningful scenario analysis requires each firm to begin by exploring those aspects of the transition that are key in view of the firm’s specific characteristics. At the end of this phase, the firm may thus feel the need to explore the evolution of various dynamics (e.g. consumer preferences for soft mobility modes; support for certain renewable energy technologies) that it will represent in its own range of scenarios. Imposing external scenarios would short-circuit the free exploration phase on key issues for the company, which is a major step in strategic thinking. When it comes to reporting on scenario analysis, standardisation is not a silver bullet.

{kind=link}

{kind=link}