Double claiming of agricultural carbon credits : time to stop worrying

In France, after seven years of the French “Low Carbon Label” (le Label bas carbone, LBC) certification scheme, there remains a systemic lack of funding for agricultural projects. The agri-food companies that would naturally be well placed to fund low-carbon agricultural projects are turning away from them and even discouraging their own suppliers from taking part in the LBC scheme.

Among the reasons mentioned by the agri-food industries is the fear of “double claiming”

Agri-food companies are concerned about being unable to account for the emissions reductions or carbon removals achieved by their suppliers in their scope 3 greenhouse gas (GHG) inventory, once these are sold to a third party through the sale of carbon credits. The GHG Protocol (GHGP) and the Science Based Targets initiative (SBTi) — two leading frameworks for private-sector decarbonisation — both restrict this “double claiming” in principle. Both frameworks require climate mitigation claims to be exclusive: the same reduction/removal cannot be claimed both by the third party financing it through a carbon credit and by an agri-food company that accounts for it in its inventory to demonstrate the achievement of its climate targets. In practice, however, the GHGP mandates adjustments only under specific circumstances. Moreover, the French regulatory framework implicitly allows double claiming.

I4CE demonstrates that the prohibition of double claiming is, most often, neither justified nor operational. It is indeed mentioned in the texts. But it goes against the very logic of scope 3 accounting. And the conditions required to trigger an accounting adjustment are rarely met.

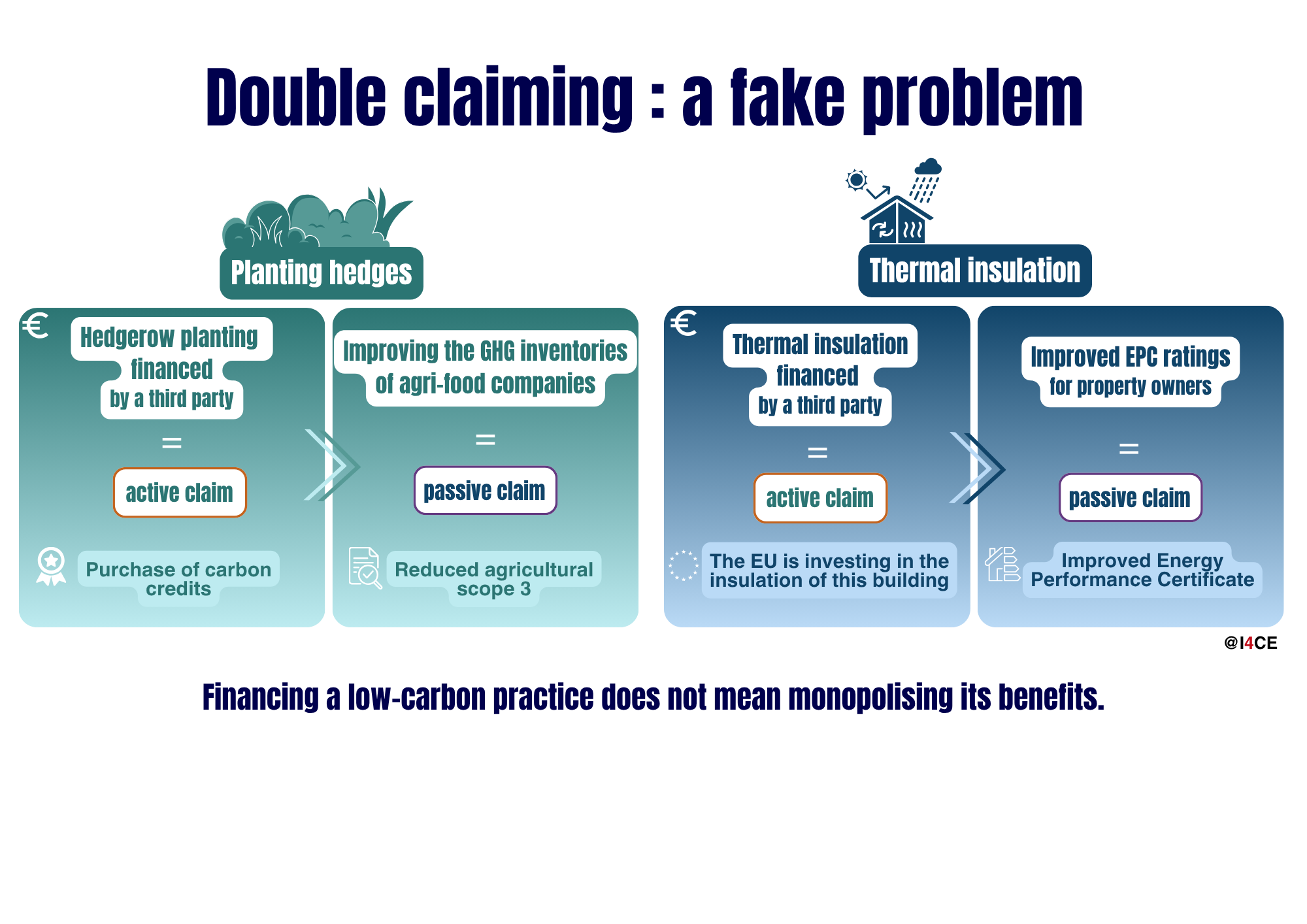

- A rule structurally ill-suited to scope 3. Scope 3 is by nature “the realm of double counting”: a reduction or removal by an upstream actor mechanically appears in the scope 3 of all its downstream clients. It is a fundamental property of this kind of accounting, explicitly recognised by the GHG Protocol itself, not an anomaly. Financing a reduction does not imply monopolizing its accounting effects. The prohibition of double claiming confuses the “active” claim made by a funder, who asserts to have made an emissions reduction or carbon removal possible, with the “passive” claim of a GHG inventory, which merely takes a snapshot of physical GHG flows.

- Tracking progress towards corporate targets is a borderline case. When a company sets a mitigation target and tracks progress via its GHG inventory, the GHGP prohibits it from counting an emissions reduction or carbon removal if the corresponding carbon credits have been sold to a third party. This is understandable. But the same logic should equally exclude reductions and removals attributable to climate change or to a supplier’s autonomous initiative, both pervasive in scope 3. I4CE favours the opposite approach: measuring progress based on physical GHG inventory, regardless of who funded the reductions or removals. This approach is imperfect in attributional terms but is both consistent and operational.

- An unworkable rule that even the standards themselves apply only under rarely met conditions. To avoid double claiming, a companyshould theoretically reintegrate into its GHG inventory the emissions corresponding to the credits sold. But this adjustment is only required when the company has precise enough data to “see” the reduction at the farm level, which is rarely the case, since agri-food inventories rely on statistical averages. Moreover, this rule is unverifiable, given the lack of physical traceability and the absence of cross-verification between credit registries and scope 3 inventories.

- A self-defeating rule penalizingfarmers. As a precaution, some agrifood companies dissuade their farmers from joining third-party carbon certification projects or impose exclusivity clauses that prevent them from accessing climate finance, without any solid legal or moral justification.

A blockage that can be overcome without delay

No legal obligation under French law requires the exclusivity of carbon claims between a scope 3 inventory and the sale of credits outside the value chain. Existing frameworks are sufficient: French regulatory GHG inventories, as well as the CSRD, already separate the GHG inventory from the disclosure of credits and project financing.

I4CE recommends that European regulations (ESRS and CRCF) clarify that an emission reduction that has generated a carbon credit may legitimately appear in the scope 3 inventory that an agri-food company publishes under the CSRD, regardless of who funded that credit. This falls under the “passive” claim, the mere observation of physical flows, and not under the “active” claim of the funder. The sale of a credit by a supplier therefore does not require its downstream clients to adjust their scope 3 inventory, and the obstacle is lifted without undermining the integrity of reporting.

|

|