Public funding for the wood sector : what contribution to climate objectives?

The new French National Low-Carbon Strategy (SNBC 3) sets ambitious targets for the forest and wood sector, yet these will be difficult to achieve as forest resources are increasingly affected by climate change and related disturbances. Maintaining and strengthening the forest carbon sink and adapting the industry to evolving forest resources are therefore key strategic challenges for the sector. However, public funding does not always align with these priorities.

This study reviews recent public funding directed towards the downstream of the forest-wood sector and assesses how it contributes to climate mitigation and adaptation. Its objective is to inform better targeting of public support in a context of tightening budget constraints.

Between 2020 and 2024, public support to the wood sector reached unprecedented levels.

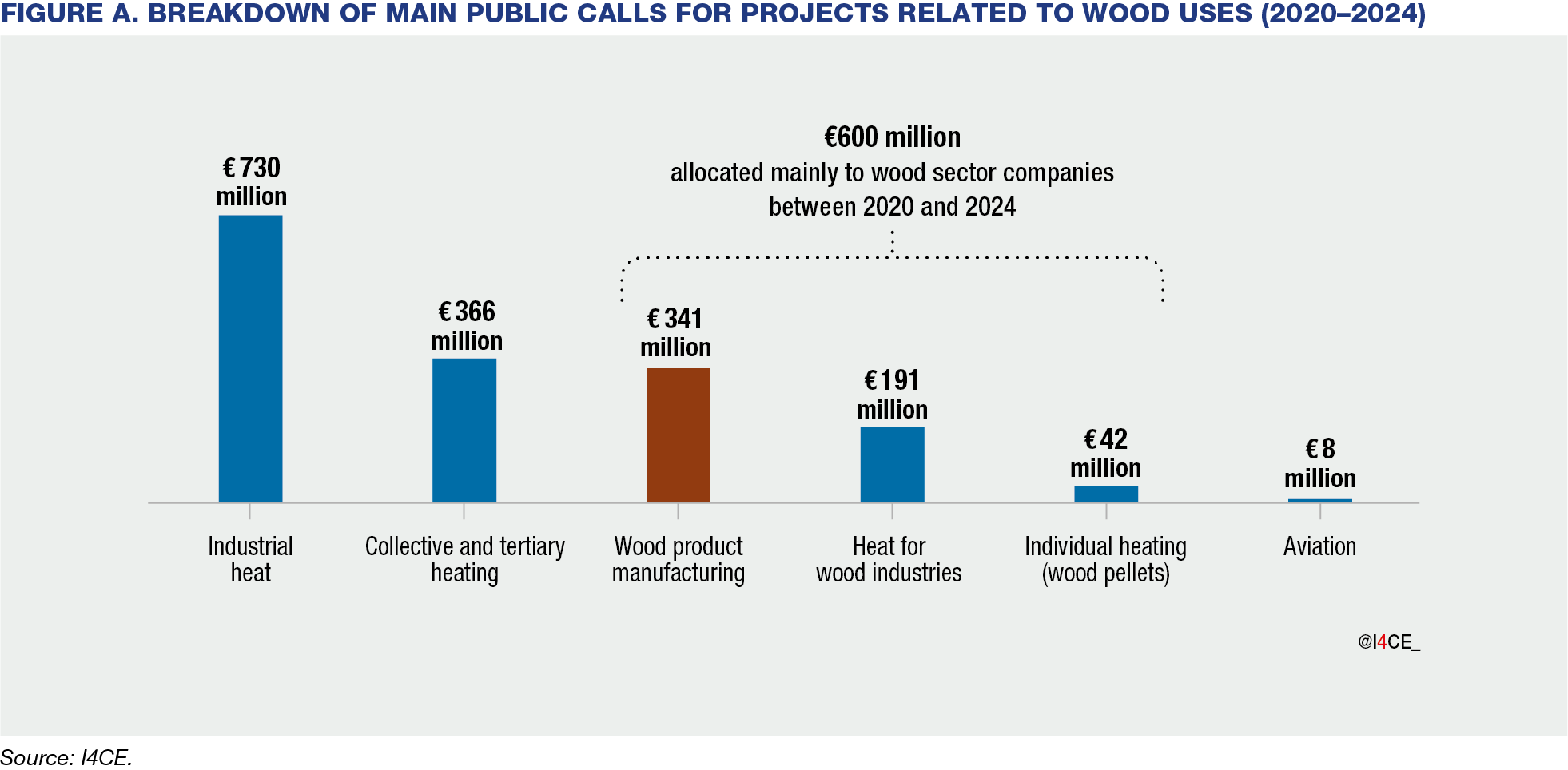

Since 2020, the wood sector has benefited from unprecedented public funding: €1.7 billion in public funding related to wood uses and allocated through calls for projects was identified over the period 2020–2024. While slightly more than €1.1 billion was mobilised for energy production outside the wood sector, nearly €600 million directly supported wood industry companies, including around €340 million for wood processing, mainly in construction (Figure A).

By comparison, over the period 2015–2018, budgetary credits specifically dedicated to wood construction amounted to €0.5 million per year according to the French Court of Auditors. This represents a clear shift in public support for the sector’s industrial development, although the balance between wood uses has changed only marginally.

€1.3 billion allocated to energy uses of wood

Public funding remains heavily concentrated on energy uses

Around 80% of total funding was directed towards energy uses, far outweighing material uses. Between 2020 and 2024, €1.3 billion in public support was allocated to energy uses (80%), compared to approximately €340 million for material uses (20%).

This strong focus on wood for energy reflects trends already identified by I4CE in 20141 and by the French Court of Auditors for the period 2015–20182, which found that energy uses accounted for around half of total public support to the whole forest-wood sector.

However, the 2020–2024 period marks a clear scaling-up: average annual support for industrial heat and collective heating increased threefold, from €72 million to €220 million. This expansion has also been accompanied by a diversification of supported uses, including new schemes for pellets and sustainable aviation fuels partly derived from woody biomass, as well as increased support for energy self-sufficiency in wood industries.

This orientation of public funding is not aligned with the cascading use principle set out in the RED III Directive, which prioritises material uses of biomass over energy uses.

Public funding partly targets priority biomass uses, but its overall allocation remains difficult to assess

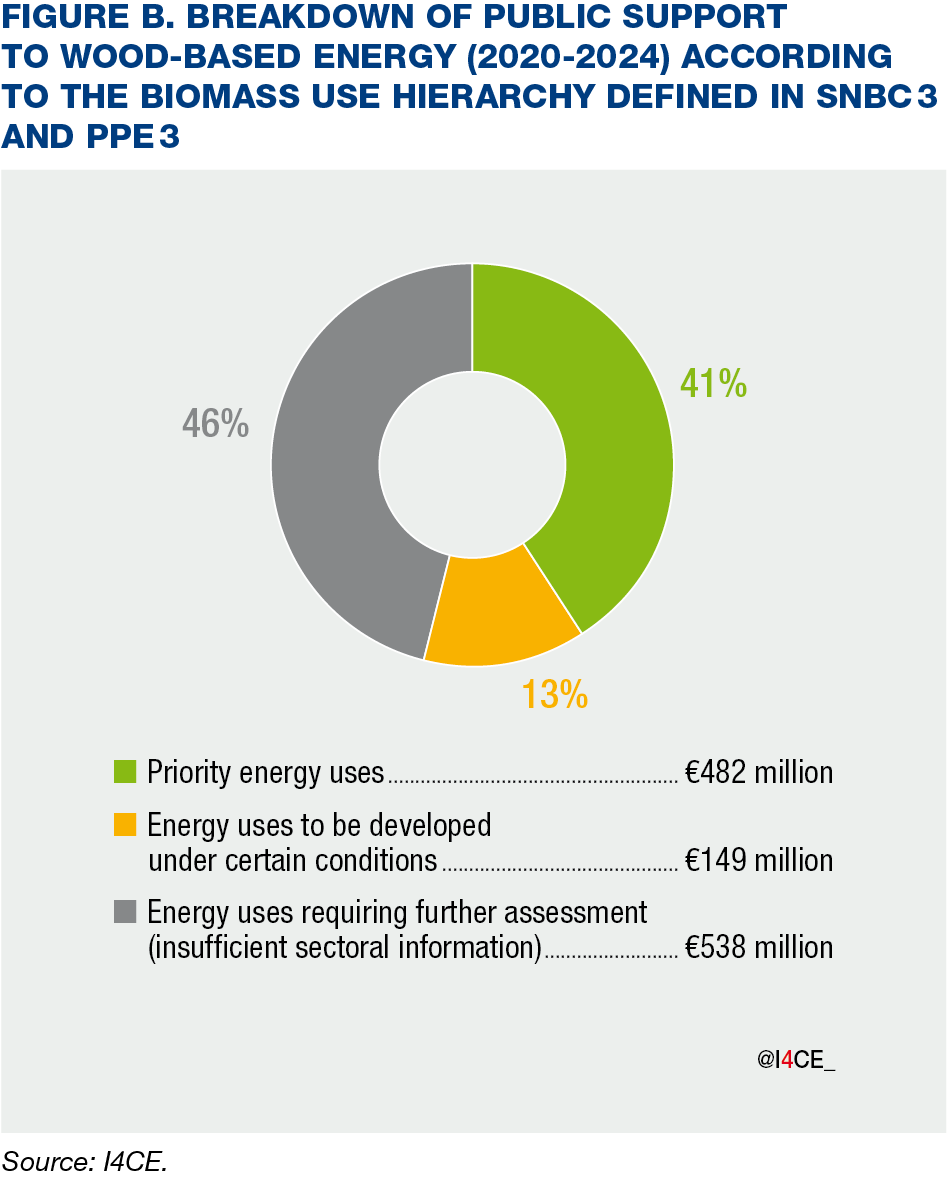

These funding schemes cover a range of situations: some support uses with no viable alternatives to biomass or that are essential to the functioning of wood industries, while others target uses for which alternatives exist. To better assess their relevance, funding was mapped against the biomass use hierarchy defined under SNBC 3 ans PPE 3.

Overall, this hierarchy appears to be broadly respected. Around 41% of funding can be linked to priority energy uses with no viable alternatives to biomass, such as high-temperature industrial heat and internal energy consumption within the forest-based sector. By contrast, only 13% of funding supports uses that should be developed more cautiously and under certain conditions, such as low-temperature industrial heat and sustainable aviation fuels (Figure B). No funding is explicitly directed towards uses considered to be limited. However, this assessment remains partial. Nearly half of the funding (46%) cannot be clearly positioned within the hierarchy, due to insufficiently detailed information on some industrial heat and collective heating projects. This points to the importance of sufficiently detailed expenditure tracking to better characterise supported uses, assess their alignment with SNBC and PPE priorities, and inform future funding decisions.

Ongoing pressure on wood resources calls into question continued support for the energy uses

Public funding for energy uses of wood, including those with limited substitution options, adds further pressure on already constrained resources, particularly on wood chips, which supply the majority of supported projects in both industry and heat networks. The wood energy production target set under the SNBC, intended to balance resource use across sectors, has already been reached.

In this context, any additional funding for energy uses further reduces the availability of wood for other uses and may create long-term lock-in effects in resource allocation. Where additional support is provided, it should prioritise uses with no viable alternatives to biomass and be complemented by stronger support for alternative decarbonisation pathways, such as electrification and geothermal energy, where available.

Recent adjustments to support schemes indicate a growing recognition of biomass constraints. These include the EnR’Choix approach3 introduced by ADEME under the Heat Fund scheme, and the introduction of caps on the use of wood chips in industrial heating projects under the BCIAT scheme. While these changes are recent, they could contribute to shifting the profile of supported projects if maintained over time.

€340 million allocated to material uses of wood

Support to wood processing industries has strengthened industrial performance, in line with the existing production model

Public support to wood processing industries has helped address part of the sector’s long-standing investment gap. It has delivered tangible improvements in industrial performance, notably by increasing production capacity and modernising processing facilities. Supported projects have also contributed to improved material efficiency and to the development of sorting and grading, both key levers for optimising the use of wood resources.

These investments largely reinforce the existing production model centred on softwood timber, which currently dominates the sector’s main end-markets, particularly in construction. Softwood accounts for around 90% of the expected additional processing volumes.

Some strategic products are nevertheless gaining momentum

These funding schemes have also supported the development of strategic products, particularly engineered wood products and wood-based insulation. They have enabled a significant scaling-up of production capacity for these higher value-added segments, which were previously underdeveloped in France, thereby contributing to reduced import dependency. For example, production capacity for insulation is expected to increase fivefold once projects are fully implemented.

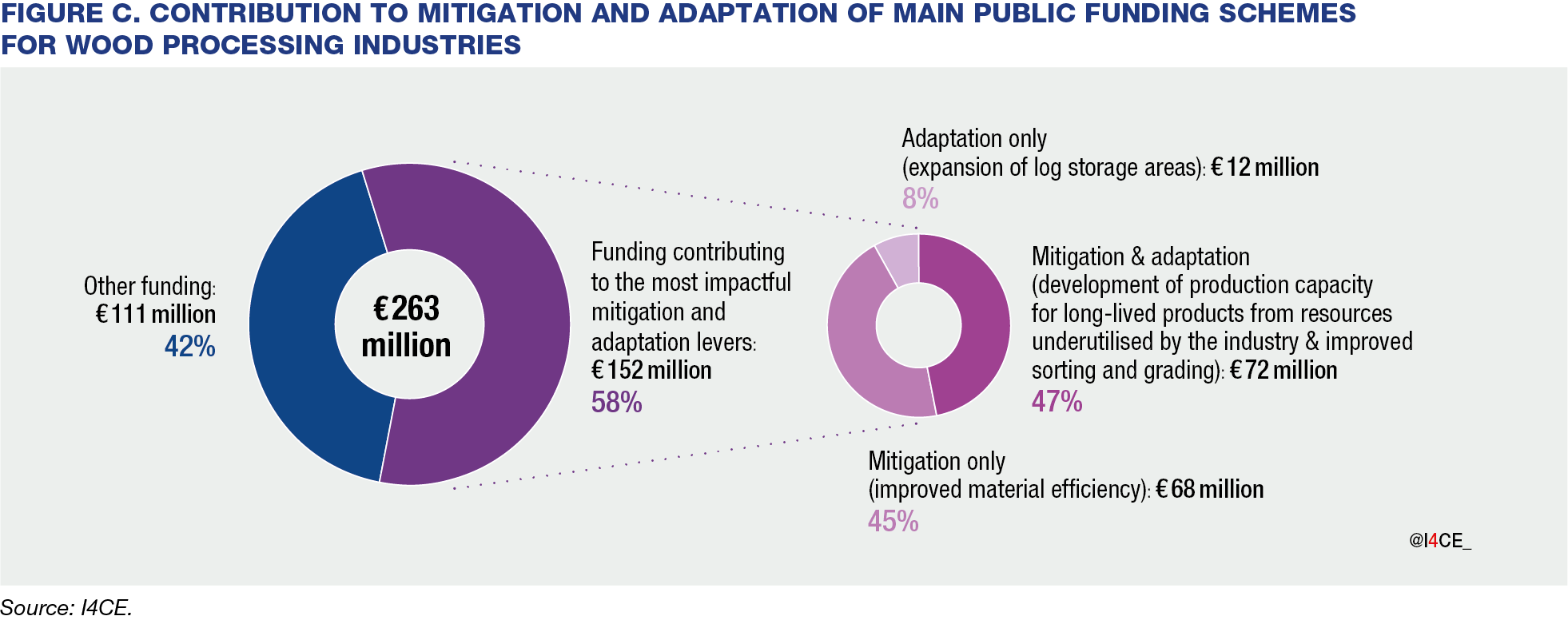

59% of the main support to material uses contributes to mitigation or adaptation

Using an analytical framework to assess how investments contribute to mitigation and adaptation in wood industries, we estimate that €152 million contributes to climate objectives, through industrial modernisation and process optimisation, as well as, to a lesser extent, through the development of processing capacity for hardwood and low-grade or small-diameter wood (Figure C). The remaining funding mainly supports the expansion of softwood processing capacity.

Funding should be maintained to support the sector’s adaptation to evolving resources

Increasing the use of hardwood and lower-grade or small-diameter wood is a key lever for both mitigation and adaptation. Currently mostly directed towards energy uses, these resources could contribute more to the carbon sink if they were transformed into long-lived products, which requires both adjustments in processing capacity and the gradual development of markets.

This challenge is likely to become more pressing as forest resources are expected to evolve, with a growing share of hardwood and lower-quality wood, potentially from salvage logging, while the relative availability of softwood may decrease.

To date, investment in hardwood processing has remained limited, although recent adjustments in support schemes point in a positive direction. The IPPB call for projects provides encouraging signals, with the latest round showing an increase in the share of hardwood (around 18%). Given the specific economic and organisational constraints associated with these resources, sustained and targeted public support will be needed to consolidate this rebalancing over time.

1 I4CE – CDC Climat Recherche. Deheza, M., N’Goran, C., Bellassen V. (2014). L’atténuation du changement climatique par les produits bois au sein des politiques françaises : priorité au bois énergie

2 Cour des comptes (2020). La structuration de la filière forêt-bois, ses performances économiques et environnementales

3 This approach aims to guide the use of biomass by encouraging project developers to prioritise energy demand reduction, waste heat recovery, and alternative renewable energy sources (such as geothermal and solar thermal), with biomass considered only as a last-resort option.