State of EU progress to climate neutrality – ECNO 2026 Flagship report

About the ECNO 2026 report

ECNO’s analysis is structured around 13 building blocks of the transition, tracking six-year trends across nearly 146 indicators, as well as the expected impact of climate-related public policies.

The transition is accelerating, but resilience depends on faster implementation

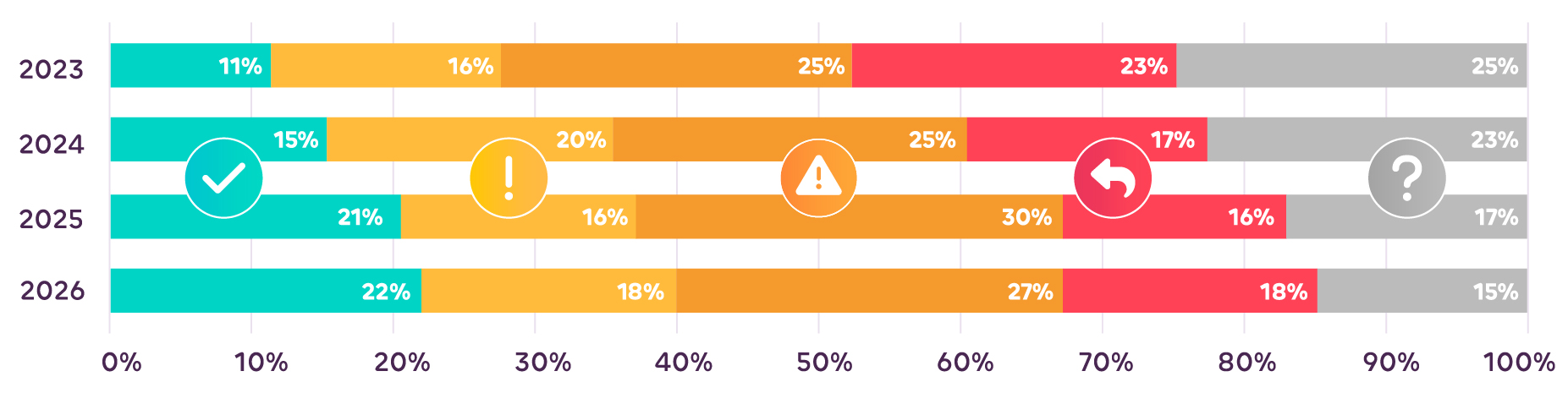

Europe’s transition to climate neutrality is accelerating and the enabling conditions for a resilient, decarbonised economy are strengthening. More than half of all indicators ECNO tracks have improved their rate of advancement compared to last year and nearly a quarter are classified as being on track to meet climate neutrality, compared to just 11% in 2023. However, our 2026 assessment also finds that progress remains uneven and overall still far too slow across most areas of the transition, leaving the EU exposed to strategic dependencies, economic vulnerabilities and worsening climate impacts.

Percentage distribution of indicator classifications in the four ECNO assessments

Percentage distribution of indicator classifications in the four ECNO assessments

Climate action is inherently tied to economic competitiveness and overall resilience

Accelerating the transition matters not only to keep climate change within safer limits, but also to strengthen Europe’s competitiveness and strategic autonomy. Recent energy crises have highlighted the economic and geopolitical risks of fossil fuel dependence, with the EU paying billions in additional fossil fuel import costs. At the same time, vulnerabilities have emerged across fertiliser supply chains, clean technology components and critical raw materials. Europe’s reliance on China for critical raw materials, battery supply chains and solar inverters creates risks, as China controls around 70% of global critical mineral refining and very large shares of most cleantech manufacturing capacities. In addition, high electricity prices – mainly driven by volatile gas markets – continue to undermine industrial competitiveness and slow the electrification needed to achieve climate neutrality across energy-related sectors.

The EU policy landscape to support the transition is still robust but increasingly uncertain

The EU’s policy landscape remains broadly supportive of climate neutrality, with a conducive policy mix in place for 85% of the overall objectives ECNO tracks and 70% for their underlying enablers. However, several key policies have been weakened. The 2035 zero emissions target for new cars and vans has been watered down, weakening investment signals for car manufacturers, and corporate sustainability reporting requirements have been significantly rolled back. Policies that actively hinder progress are rare, but the agrifood sector is a notable exception, where Common Agricultural Policy subsidies continue to favour emissions-intensive livestock farming over more sustainable models.

Amidst this backdrop, safeguarding some of the EU’s flagship policies, such as the EU ETS and using the current energy security challenges as a catalyst for faster climate action become essential. Strengthening resilience and accelerating the transition must increasingly be seen as complementary objectives.

As the EU develops its post-2030 climate and energy framework, the decisions taken in the coming months and years will determine whether the transition to climate neutrality strengthens Europe’s resilience and competitiveness, or whether structural vulnerabilities are locked in for another decade.

Highlights where the transition is heading the right way

In some areas, we see positive developments to support the move to a resilient, climate neutral future. These include the following ones worth noting:

-

Transport and buildings are showing signs of acceleration. Zero-emission vehicle (ZEV) registrations reached a record high in 2025, with the trend increasing further in the first half of 2026, while the share of rail passenger transport has seen a moderate increase. Heat pump sales partly recovered in 2025 and demand for heating and cooling is falling faster than in last year’s assessment. The share of energy subsidies for energy efficiency purposes doubled between 2021 and 2024.

-

Citizens are increasingly shaping the transition, while regional poverty is declining. Cattle meat consumption continues to decline beyond official expectations, and for the first time this year, so does dairy consumption – despite few or no policy incentives in place. Poverty reduction across EU regions most vulnerable to the energy transition is now on track to reach the EU’s overall target of reducing poverty by at least 15 million by 2030.

-

The EU expanded its international climate finance contributions. Public finance for international clean energy projects by the EIB and climate-related official development assistance both increased, strengthening our assessment on the EU’s external climate action.

Areas that require increased attention

At the same time, overall progress remains uneven and the outlook has stalled or worsened in several critical areas. For the first time since ECNO’s tracking began in 2023, none of the 13 building blocks of the transition are on track. Several areas have seen a worsening outlook:

-

Weak cleantech investment is undermining industrial resilience. After briefly reaching an “on track” classification last year, the EU’s cleantech ecosystem is once again developing too slowly, with sustained declines in public energy and environmental R&D spending and cleantech scale-up investment.

-

Finance is heading the wrong way, failing to support the transition. Financial flows remain vastly misaligned with climate goals due to a lack of investment in critical areas for the transition, while fossil fuel subsidies remain high.

-

Nature-based resilience continues to deteriorate. The overall state of carbon dioxide removal has worsened and is again moving in the wrong direction, driven by slowing growth in EU forest area and declining carbon stocks.

Priority actions

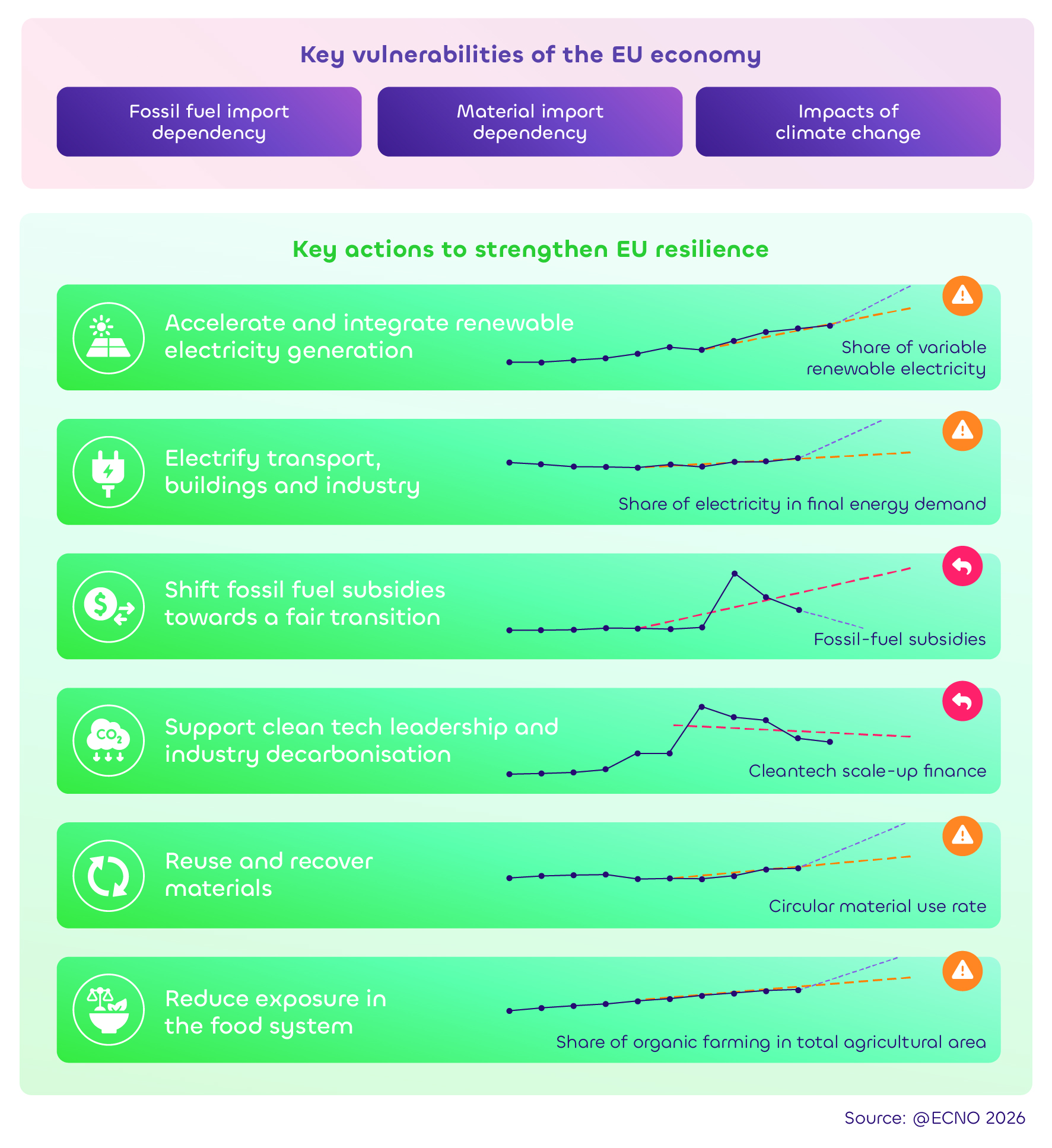

Accelerate renewable electricity generation and grid integration

Variable renewables stood at just 30% of electricity generation in 2025, rising far too slowly to meet the 58% deployment needed by 2030. Wind buildout is lagging in particular. Grid investment, battery storage and smart meter rollout all remain insufficient. Faster permitting, more integrated grid planning and stronger incentives for non-fossil flexibility are needed to scale up renewables to the levels needed.

Electrify transport, buildings and industry

Electrification rates have stagnated at just over 20% for a decade. Closing the electricity-to-gas price gap, including through energy taxation reform and stronger policy support for batteries, heat pumps and electric vehicles, is essential to make electrification commercially viable across sectors.

Redirect fossil fuel subsidies towards a fair transition

Fossil fuel subsidies remain high at nearly EUR 100 billion. Broad energy price relief should be replaced with targeted support for vulnerable households, combined with investment in building renovation, heat pumps and affordable public transport. The Social Climate Fund is a key opportunity that Member States must use effectively.

Support cleantech leadership and industrial transformation

Europe risks falling behind in the global clean technology race. Large-scale cleantech investment halved from EUR 10 billion in 2021 to EUR 5 billion in 2025, while public R&D spending has plummeted. In heavy industry, there is a stark funding gap for CO2 transport and storage: current public funding is around EUR 300 million against an estimated need of up to EUR 23 billion. A broader industrial strategy is needed that combines carbon pricing with stronger demand creation, de-risking instruments and measures to reduce supply chain dependencies on China.

Strengthen circularity and material recovery

Europe is becoming more resource-efficient, but only 12% of materials are recycled back into the economy. This share needs to rise sharply as demand for critical raw materials tied to clean technology grows. The forthcoming Circular Economy Act should translate ambition into binding market creation, including stronger recycled content standards and circularity criteria in public procurement.

Reduce vulnerabilities in the food system

European agriculture remains highly exposed to climate impacts, fertiliser price volatility and fossil fuel dependence. Structural change is needed to build long-term resilience, including reforming CAP subsidies to support more sustainable farming models, further reducing synthetic fertiliser use and expanding organic farming area, which needs to go up from around 11% currently to 25% in 2030.

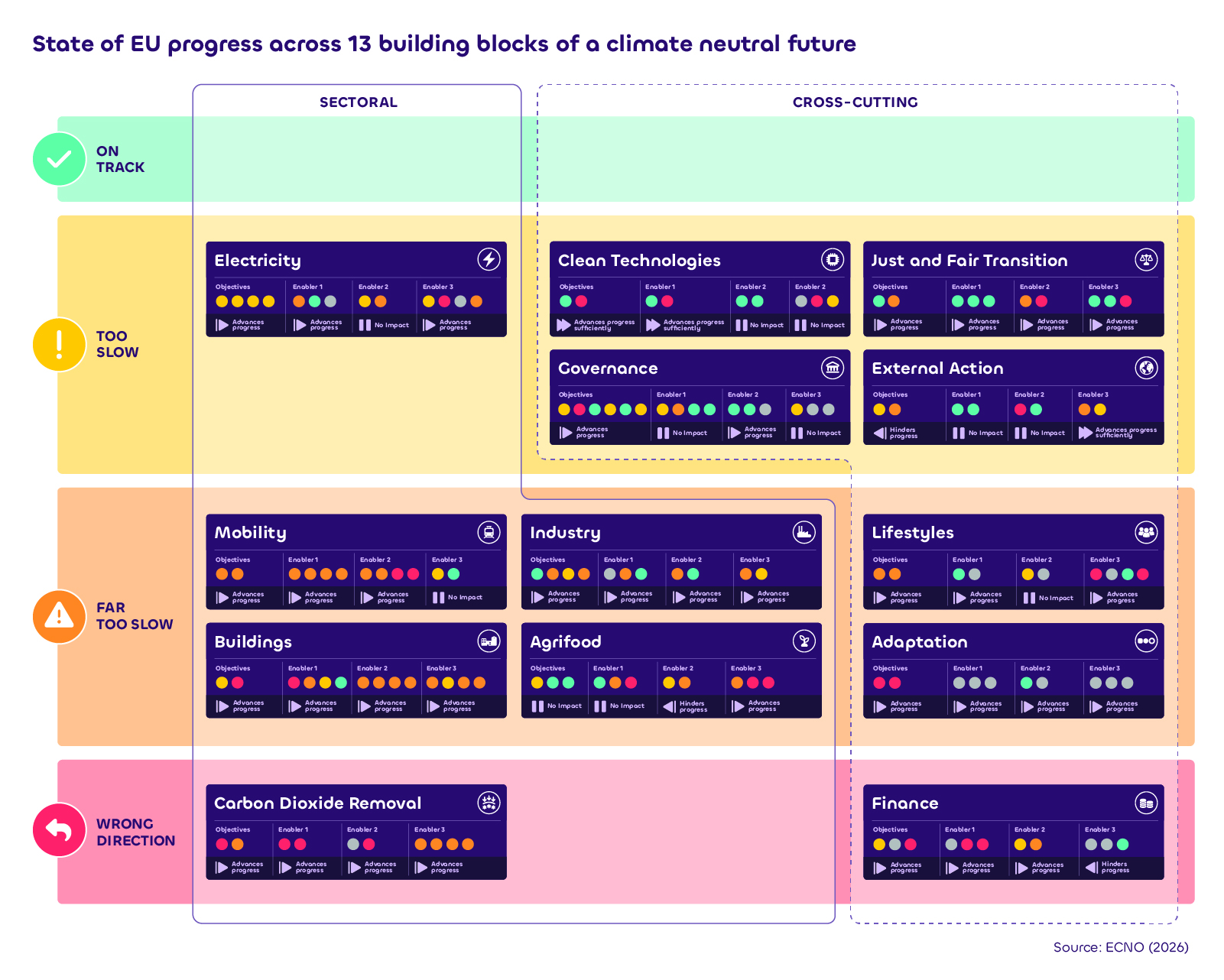

Headline results across 13 building blocks

At building block level, the results point not to uniform stagnation, but to an uneven transition. Positive developments are visible in several areas, even where they are not yet strong enough to change the overall classification of a building block.

Compared to last year’s assessment, External Action improved its classification from far too slow to too slow thanks to increases in the EU’s climate-related official development finance and finance for international clean energy projects by the European Investment Bank.

Buildings, Mobility, Agrifood and Just and Fair Transition saw positive indicator-level developments, including, among others, recovering heat pump sales, record ZEV registrations, declining dairy consumption and improved trends in regional poverty in areas most vulnerable to the transition – although these gains were not yet broad or fast enough to improve their overall building-block classifications.

These developments matter because they show that parts of the transition are responding to policy, market signals and citizen choices. The overall picture is therefore not one of stalled progress, but one that remains too uneven and too slow to put the EU on a secure path to climate neutrality.

Reversals show that earlier gains are not yet locked in

The assessment also shows that momentum remains fragile. Finance continues to move in the wrong direction, although the decline in fossil fuel subsidies after the 2022 crisis peak shows that part of the emergency support is being withdrawn – at least in 2025. This confirms Finance as a persistent weakness across ECNO’s assessments, with financial flows still not aligned with the investment needs of the transition.

Two building blocks show concerning reversals in their overall classification. Carbon Dioxide Removal has shifted back into heading in the wrong direction due to declining growth rates for forest area and carbon stocks, while technical removals continue to develop from a very low base. Clean Technologies has slowed after being on track last year following a decline in large-scale cleantech investment with, for example, many planned battery gigafactories cancelled or delayed. In addition, public environmental and energy R&D funding has fallen to its lowest level since 2015, and EU policies to support bringing innovation to market, and increasing clean technology uptake have only a limited impact. These reversals are particularly notable because both building blocks had improved in the 2025 assessment compared with 2023 and 2024, underlining that previous progress was not yet sufficiently established.

Overall, Electricity, Mobility, Industry, Buildings, Agrifood, Lifestyles, Just and Fair Transition, Governance, and Adaptation retained their previous classifications, with progress still too slow or far too slow.