“Green budgeting”: paths to creating real added value

Few green budgeting initiatives have led to concrete reforms or revisions of priority investments. How can we move from simple theoretical exercises to concrete action for the environment? This is the question asked by Sébastien Postic of I4CE, Oskar Lecuyer of AFD and Jennifer Doherty-Bigara of the Inter-American Development Bank (IDB).

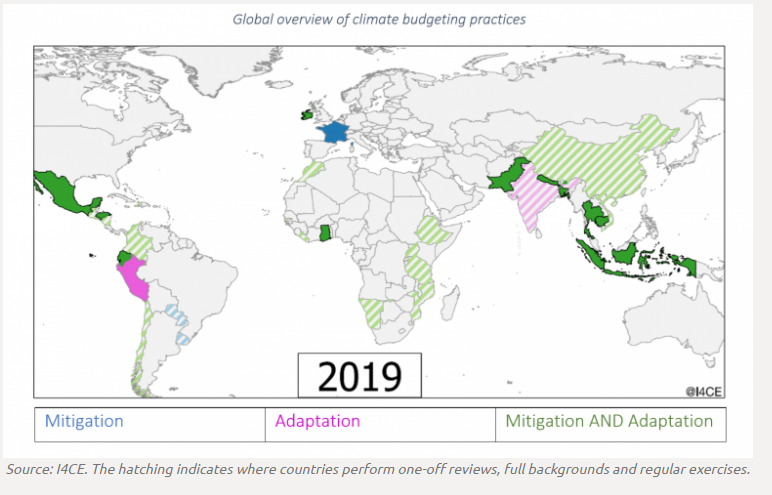

One year ago, on September 25, 2019, France announced that 10% of its expenditure, €35 billion, would be spent to benefit the environment. This figure was determined during the first national “green budgeting” exercise, with other climate-based reviews taking place in Nepal (27% of expenditure to benefit the environment in 2018), in Guatemala (1.6% in 2018), in Kiribati (20% in 2018), and even in the Indian State of Odisha (31% in 2019), and so on. In total, more than 50 countries have already produced such analyses (see map below). It is, therefore, common practice, however, the tools available are still in their infancy, and there is little standardization among them, a fact illustrated by the significantly different figures produced.

What is green budgeting? What is its purpose? These questions will be briefly discussed here, before identifying a range of criteria that must be applied for these exercises to be truly useful. The real challenge is to ensure that green budgeting represents more than just a theoretical exercise, and that real progress is made in taking the environment into account when preparing public budgets.

Click on this button to see the image

What is green budgeting?

The term “green budgeting” covers a variety of practices aimed at identifying and assessing elements of the public budget that affect one or more aspects of a State’s environmental policy. For example, public expenditure can be identified which contributes to either mitigation of or adaptation to climate change, as well as to the fight against artificialization of land and to the protection of biodiversity. Certain green budgeting exercises encompass expenditure that is damaging to the environment, such as subsidies for fossil fuels, and other types also analyze public revenue, or have an even broader scope to include other public entities (i.e. government agencies and local authorities).

As a result, these exercises can vary considerably in form. Although some standards such as the Climate Public Expenditure and Institutional Review (CPEIR) have been replicated in many countries, there is no universal definition of green budgeting today, let alone a universal “blueprint”. The objectives of such reviews can also differ widely: from aiming to simply identify expenditure to applying a weighting to different types of expenditure according to their “relevance”.

Why produce a green budget?

As a first approach, an exercise in green budgeting can be defined as having three objectives. The first is to facilitate budget steering. The identification of environmentally-friendly expenditure, or that which is damaging to the environment, represents the first step before analyzing its effectiveness, the options for reform, additional financing needs and, more generally, its consistency with the country’s climate change objectives.

Green budgeting also contributes to the skills development of administrations, not just for public experts in terms of environmental issues, but also for environmental specialists in budgetary matters.

Finally, it improves transparency. The results enable better understanding and improved evaluation of government policy, not only for the executive and parliament members, but also for civil society and citizens.

The case for internal, recurrent budget exercises

In view of the objectives described above, certain criteria emerge as essential for a green budgeting exercise to create added value, and they largely relate to taking ownership of the process.

At the top of the list is the need for recurrent exercises, in line with existing budgetary processes, to improve the steering of climate change policy, and which must be performed internally to be appropriated by governments.

Unfortunately, in practice, less than a third of the countries listed above analyze their budgets on a recurrent basis. These exercises are generally instigated by development agencies or international donors, in the context of limited, one-off, externally funded projects, and are often outsourced to independent consultants. Although this may be necessary as a starting point, this arrangement does not ensure much involvement from governments and thus limits the development of their skills in this field.

Finance and the environment, the need for close collaboration

The second essential condition is close collaboration between ministries, which implies that the roles of finance and environment ministries must be redefined. Almost everywhere in the world, environment ministries have historically managed all environmental issues, including fiscal matters, as demonstrated by the global experience with carbon taxes, and negotiations on climate change financing.

As climate change initiatives and the related financial challenges continue to multiply, this situation must change, and is changing, as recent initiatives such as the Coalition of Finance Ministers for Climate Action. have shown. Therefore, the involvement of finance ministries in green budgeting exercises is, at the same time, a necessity because their expertise in these technical subjects is vital. This seems obvious, as they are on the front line in terms of effective budget management and it provides an opportunity for them to develop their skills in environmental issues.

Environment ministries, for their part, have invaluable technical expertise which is essential if countries are to be involved in global climate change initiatives. Consequently, green budgeting requires close collaboration between these two different types of ministry.

Green budgeting: a tool for decision making!

Finally, if green budgeting does not result in a change of approach to climate change in terms of public budgets, it has failed its primary objective. Communication is, of course, fundamental: it is important that indicators are defined but they must also be communicated to the executive, members of Parliament, and civil society. In this respect, the publications produced by Bangladesh for the general public, for example, should be applauded.

And yet these efforts do not go far enough. It should be noted that few green budgets have resulted in concrete reforms on environmentally-damaging expenditure, or in an analysis of the effectiveness of environmentally-friendly measures. Governments rarely take full ownership of these exercises, a prerequisite for their transformative potential, and thus their usefulness. I4CE and AFD are currently working on this field of research.

The environment: what should be done in times of crisis?

In conclusion, the latest figures are telling: despite calls and commitments to build the “world of tomorrow”, one that is more respectful of people and the environment, the support and recovery measures adopted by G20 countries in response to Covid-19 amount to $205.6 billion for fossil fuels, compared to $135.91 billion for renewable energies and energy efficiency. This is an emergency response, and yet it is still an improvement on the recovery package in 2008.

However, whether the political will is there or not, tools to help develop emergency solutions that do not undermine climate initiatives are in short supply. Green budgeting, with the global vision it can provide, should be seen as one such tool.

{kind=link}