Reporting d’entreprise et analyse par scénarios : standardisation n’est pas raison

La Commission européenne a ouvert depuis quelques mois une consultation pour la révision de la Directive sur le reporting extra-financier. L’enjeu : renforcer l’obligation de 6 000 grandes entreprises à communiquer publiquement sur leur façon de traiter des questions sociétales majeures, comme le changement climatique et la transition bas-carbone. Pour Romain Hubert d’I4CE, le reporting doit en particulier être renforcé sur les analyses par scénarios que mènent les entreprises pour identifier les risques et opportunités de la transition. Mais que devraient-elles communiquer exactement ?

Voici nos recommandations, d’après notre dernier rapport de recherche, en faveur d’un reporting obligatoire au sujet de l’analyse par scénarios sur les risques et opportunités de la transition.

L’analyse par scénarios, un exercice indispensable

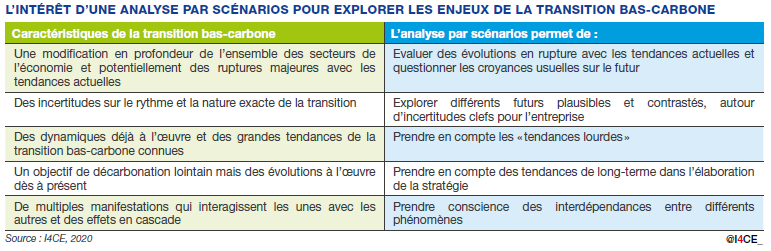

Pour réduire drastiquement leurs émissions de gaz à effet de serre et atteindre la neutralité carbone, l’ensemble des secteurs de l’économie vont devoir se transformer en profondeur. Cette transition vers un monde bas-carbone expose les entreprises à des risques et à des opportunités stratégiques dans leur environnement d’affaires, d’autant plus difficiles à appréhender qu’il existe de nombreuses incertitudes sur l’ampleur des efforts qui seront mis en œuvre pour la transition, sur leur timing et leurs modalités.

Dans ce contexte, « l’analyse par scénarios » se révèle être un outil très utile aux entreprises pour explorer les enjeux concrets de la transition bas-carbone et construire une stratégie résiliente aux futurs possibles. Cet exercice est d’ailleurs recommandé par le groupe d’experts de la TCFD, et certaines entreprises – trop peu – mènent déjà ce genre d’analyse. L’analyse par scénarios est utile aux entreprises elles-mêmes, et elle l’est aussi à leurs parties prenantes financières : banquiers, investisseurs, etc. Les acteurs financiers ont besoin d’en savoir plus sur ces analyses menées par les entreprises, pour mesurer en quoi les entreprises qu’ils financent les exposent, eux aussi, à des risques et opportunités en lien avec la transition.

Cliquez sur ce bouton pour voir l’image

Il faut renforcer l’obligation de reporting

Le reporting extra-financier des entreprises est un canal de communication possible entre entreprises et acteurs financiers sur l’analyse par scénario, comme le souligne la TCFD. Mais la directive qui encadre ce reporting au niveau européen, la NFRD pour Non financial reporting directive, ne fait que mentionner ce type d’analyse dans ses lignes directrices non contraignantes. Les entreprises sont donc simplement invitées à aborder le sujet de l’analyse par scénario dans le reporting destiné à leurs parties prenantes financières, sans être obligées de le faire. La révision de la NRFD est l’occasion de changer cela.

L’obligation de reporting est pertinente en premier lieu pour stimuler les entreprises à mettre en œuvre l’analyse par scénarios, et prendre des décisions qui améliorent la résilience de leurs stratégies. Nous constatons en effet que trop peu d’entreprises mettent en œuvre l’analyse par scénarios actuellement. Pourtant de nombreuses ressources existent pour guider les entreprises dans cette démarche stratégique, à hauteur des moyens qu’elles peuvent y consacrer. Elle peuvent s’appuyer par exemple sur le rapport qu’I4CE a publié pour aider les entreprises à se familiariser avec les scénarios de transition bas-carbone , ou sur notre tout nouveau guide pratique sur l’analyse par scénarios, présentant des fiches méthodologiques, outils en ligne, travaux prospectifs sectoriels, etc.

L’obligation de reporting est également nécessaire pour aider les entreprises à franchir le pas d’une communication publique sur ces analyses. Nombre d’entre elles bloquent sur l’enjeu de confidentialité associé à cette analyse d’intérêt stratégique. Nous avons pourtant constaté, en rédigeant notre guide pratique, que certaines entreprises incluent déjà des éléments sur cette démarche dans leur reporting. Il faut donc dédramatiser cet enjeu de la confidentialité ! Les entreprises doivent faire la part des choses. Elles peuvent recenser l’information qu’elles divulguent déjà, et réfléchir à la sélection d’information et aux formats de présentation qui lui permettront de communiquer les points importants de l’analyse sans trahir ses enjeux de confidentialité.

Attention à la standardisation du reporting sur l’analyse par scénarios

L’obligation de reporting sur l’analyse par scénarios nous semble donc nécessaire…. Concrètement, que devraient communiquer les entreprises à leurs parties prenantes financières ? Les acteurs financiers ont tendance à demander des informations extra-financières comparables entre entreprises, et la Commission suggère une forme de standardisation du reporting extra-financier. Mais en matière de reporting sur l’analyse par scénarios, il faut se méfier de la standardisation à tout prix !

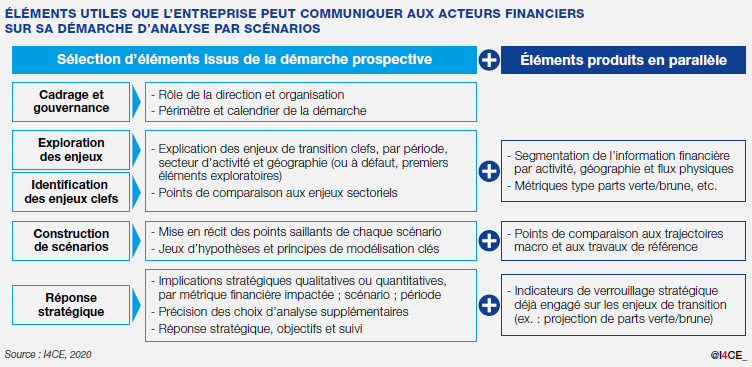

Nos travaux montrent que les acteurs financiers souhaitent surtout comprendre la démarche de l’entreprise, et apprécier la solidité de son approche. Où en est l’entreprise dans la prise en compte des enjeux de la transition bas-carbone ? Comment détermine-t-elle ses enjeux clefs dits « matériels » ? Comment explore-t-elle ses enjeux stratégiques sur les horizons proches et éloignés ? Apporte-t-elle une réponse stratégique adéquate ? Pour ce faire, la standardisation du reporting devrait porter sur l’obligation d’évoquer systématiquement un certain nombre d’aspects de l’analyse par scénarios (cf le tableau ci-dessous). Ils devront être communiqués par étape en fonction du rythme de progression de l’entreprise dans sa démarche d’analyse.

Ainsi, il est particulièrement utile que l’entreprise communique dès le départ sur la phase de cadrage de sa démarche, afin d’expliquer comment elle construit une capacité à intégrer l’analyse prospective dans sa prise de décision stratégique. Il peut s’agir d’un calendrier de mise en œuvre, avec les différentes étapes, objectifs et rôles des personnes impliquées – notamment la direction et le Conseil d’administration, et l’articulation avec les processus habituels qui alimentent la réflexion stratégique.

Notons que les acteurs financiers apprécieront que l’entreprise fournisse aussi des informations complémentaires, comme des points de comparaison avec des travaux connus (ex. en quoi les scénarios de l’entreprise se rapprochent de scénarios de l’AIE connus en finance, ou des quatre grands narratifs de transition formulés par le NGFS).

Cliquez sur ce bouton pour voir l’image

Ce qu’il ne faut pas standardiser par contre, ce sont les scénarios à utiliser par les entreprises. Il serait contre-productif de leur imposer des scénarios standardisés, sur lesquels elles devraient fonder leurs décisions stratégiques. Cette tentation est grande car des scénarios communs apporteraient une comparabilité aux analyses des multiples entreprises que les acteurs financiers doivent examiner. Mais une analyse par scénarios pertinente demande à chaque entreprise de commencer par explorer les aspects de la transition qui sont clefs aux vues des caractéristiques propres à l’entreprise. A l’issue de cette phase, l’entreprise peut ainsi éprouver le besoin d’explorer l’évolution de dynamiques variées (ex. les préférences des consommateurs pour des modes de mobilité douce ; un soutien à certaines technologies de production d’énergies renouvelables) qu’elle représentera dans sa propre gamme de scénarios. Imposer des scénarios externes reviendrait à court-circuiter la phase d’exploration libre sur les enjeux clefs pour l’entreprise, alors que c’est une étape majeure de la réflexion stratégique. En matière de reporting sur l’analyse par scénarios, standardisation n’est pas raison.

{kind=link}

{kind=link}